The plan asset rule, among other things, is used to determine whether or not a retirement plan is involved in a prohibited transaction.

A PT happens when a plan enters into a transaction with a disqualified person. In our previous post, we covered how to make a list of disqualified persons for a specific plan. This included determining whether a partnership, LLC, corporation (or other entity) is a DQP itself because of significant ownership by other DQPs.

A prohibited transaction occurs when all three factors are present: a DQP, a plan, and a transaction between the two. So, from the previous post we know how to determine if an entity is considered to be a DQP itself. But how do we know if an entity is considered to be a plan?

Plan asset look-through

…is the term DOL uses (The U.S. Department of Labor, DOL, is the government entity that solely has the authority and responsibility to interpret prohibited transactions code). If a situation does have plan asset look-through it means that you look through an entity to the plan and consider the assets of the entity to be the assets of the plan itself. This also means that when you do have plan asset look-through, that entity is treated as if it is the plan itself for PT purposes. That would mean that that entity could not transact with a disqualified person.

When is there plan asset look-through?

The first hard and fast rule is that when an entity is owned 100% by a plan, there is plan asset look-through. So if your Solo 401(k) was 100% owner of an LLC (or any other type of entity) then that LLC would be seen as if it were the plan itself for purposes of PT determination.

The second rule is that when a plan owns 25% or more of an entity, there is plan asset look-through. I know you have a scrunched up face right now because the second rule seemingly makes the first rule unnecessary. This second rule isn’t hard and fast like the first rule. This rule does not apply if you have an “operating company”.

What is an operating company?

This is where the fun starts.

An operating company is one that primarily makes or sells a product or service other than the investment of money.

A real estate operating company is one where at least 50% of its assets (valued at cost) are invested into managed real estate or real estate development, provided that the entity is directly engaged in the management or development activities.

So, back to plan asset look-through… If you have an operating company, the there is only look through if a plan owns 100% of the operating company. If you don’t have an operating company, there is look through if the plan owns 25% or more of the company.

At first glance you may think “wow, there are some major benefits to investing in an operating company”. I partially disagree. Firstly, your plan is intended for passive investment. An operating company suggests that its owners are engaging in a business activity which might subject the plan to UBIT tax (35% tax on almost all of the income from the entity rather than just the income attributable to leveraged) and it might even create a PT if the accountholder/participant is engaged in the management or development activities. You see, a plan can’t operate a business, so if it owns something that is a business, the reality is that the plan’s accountholder or participant is operating the business, and that is a no-no.

Secondly, the only benefit to intentionally creating an operating company for the purposes of skirting the plan asset rule would be if you intend to involve a DQP with your plan. That intent alone starts you off on the wrong foot.

To simplify, an entity is a plan if significantly (25% or more) owned by a plan. An entity is a DQP if it is significantly (50% or more) owned by other DQPs.

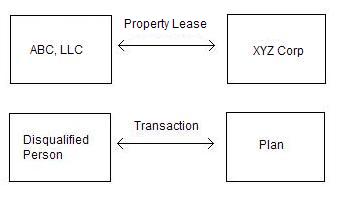

Let’s use an example. XYZ Corp is 35% owned by Rachel’s IRA. Rachel’s mother owns 60% of ABC, LLC. Rachel and her mom are thinking of directing XYZ to lease a property it owns to ABC, LLC. Because of the significant ownership on both sides, this is what it looks like:

| ABC, LLC | XYZ Corp | |

| Owned 60% by Rachel’s mother | Owned 35% by Rachel’s IRA | |

|

||

…and it is a prohibited transaction. Some people even go to the extent of officially requesting a PT exception from DOL in order to execute a transaction such as this. To me, this is silly. DOL would only consider granting such an exception if the lease were for market value to ensure that a DQP isn’t getting special use of plan assets or vice versa. If the proposed lease were for market value, then ABC, LLC shouldn’t have a problem finding another leasee who isn’t a DQP. With the same logic, XYZ Corp shouldn’t have a problem finding another leasor who isn’t a plan. All things considered, this type of transaction should just be avoided completely.

Finding out if a proposed transaction is possibly a PT should follow this simple process:

- Is there a plan? (follow the plan asset look-through rules) If yes, continue to next question…

- Is there a disqualified person? (refer to the DQP list you made) If yes, continue to next question…

- Is there a transaction between the two? If yes, you probably have a PT; don’t follow through with it.

I would follow that actual order so that you can reach your answer as quick as possible. There’s no harm in walking away from a transaction because it might be prohibited, but inversely if you are pretty sure something is not a PT, but there is a DQP involved somewhere/somehow… check with a qualified attorney before proceeding.

Following that step by step process to attain the peace of mind that your transactions are building your wealth rather than risking it to hefty tax penalties.